The value of a company can be determined by summation of all future cash flows while discounting at a realistic rate.

When you invest your money in stocks today you have to apply a discount rate as a kind of compensation and safety buffer and this consequently influences the calculation of a company’s value. But what will be a fair interest rate you can call for when purchasing stocks of a company?

There are different possible approaches.

First for example you can use the price-earnings ratio (PER) partially for determining the discount rate by making use of the reciprocal of the price-earnings ratios. The shareholder receives his interest return in form of corporate profits .

For example a PE ratio of 20 corresponds to an interest rate of 1/20 = 5%.

However, the profits of companies are not constant. Counteracting rising or falling profits, you need to adjust the “fair” PER slightly up or down. But ultimately it all comes down to an abbreviated discounted cash flow method.

Determination of CAPM

The modern economics have developed a model to solve this question which is named the Capital Asset Pricing Model (CAPM). The basic idea of the model is the hypothesis that the risk of an investment in equities is represented by the fluctuation of the stock price. To handle a greater risk a higher interest rate must be applied in return.

But this model also contains handicaps inter alia on the assumption that the price fluctuation of a stock is a direct measure of the risk of the investment.

Value investing is more likely based on the assumption that while investing in stocks risks are derived from how the company is managed and from the company’s fundamental health and not purely and solely from fluctuations of the stock price traded at the market.

Relevant literature is concerned with the criticism of the CAPM .

The approach of PURE Rating

Now we would like to address ourselves to the question of determination of a fair discount rate. John Burr Williams recommends in his book, published 1938, named “The Theory of Investment Value”, that every investor should use his own personal interest rate to determine the intrinsic value of a company.

You should also take into account the average interest rate other market participants will call for in the future when determining the discount rate for equity investors.

- The following questions have to be answered:

- What rate of return should be required when trading equities at the stock market

- What is the average interest rate market participants generally call for in the future

Of course, these questions also relate to each other and must be assessed realistically to survive in the future stock market even when selling these assets later.

Inflation

Each interest payment below the rate of inflation is unacceptable to us. Thus the long-term average will most likely not be lower than the present ECB inflation target of about 2%.

Money market interest payment

Based on a currently anticipated interest rate of 1% p.a. and the fact we have to pay tax compensation we will set the minimum return to 2%.

The sum of compensation for inflation and interest payments is now already at 4%.

Bond yields

When analyzing the bond market more than 4% return is quite possible, even with relatively safe bonds. With bonds the risk may also be significantly lower, compared with the related stock.

First the bond holders receive their interest returns, thereafter the remainder of the profits will be paid to shareholders. Even in the event of insolvency, the shareholders receive only what is left after the bondholders have been paid. So bonds make sense if the expected return is higher than the stock’s return.

Because stocks naturally have an infinite maturity, it makes sense to use long-term bonds for comparison.

For this we take a look at the yield curve of the Stuttgart Stock Exchange and considering bonds only with a residual maturity of over 10 years. On average, these type of assets yield the following:

- Bunds 2,195%

- Corporate bonds (AA) 2,767%

- Corporate bonds (A) 2,962%

- Corporate bonds (BBB) 3,492%

As of October 2013

Government bonds with top ratings, so as German bunds are, are considered as very safe by the market, as well as corporate bonds with different ratings of e.g. S&P. BBB rated bonds are just still among the ratings of “investment grade” and are considered so as to be “non- speculative”.

Due to a variety of reasons in general stocks can basically classified as a more insecure asset compared to BBB rated bonds or better. With the BBB rating bonds of e.g. Bayer, Daimler, German Telekom, K+S, Linde, Metro and Siemens were classified.

In so far we could consider 4% as an absolute lowest limit for our asset returns.

Bond yields in the past

Bond yields presently quote at a historically low level. This is true for short-and long-term bonds. Yields on BBB-rated corporate bonds have quite been profitable even in the recent past returning about 7%.

Bonus for risk

We therefore assume that BBB-rated long term corporate bonds may result in a return of 4-7 %. Their interest payments are considered to be relatively safe.

Profits of even stable companies are difficult to predict for the future, especially since more and more tricks of accounting are applied. Fluctuating company profits thus require a risk bonus or a higher interest rate as an compensation.

How high should the risk bonus be?

For very stable companies that are well analyzed, 1% might be enough to start with. A more conservative and cautious consideration requires rather a surcharge of 5, 6 or more percent.

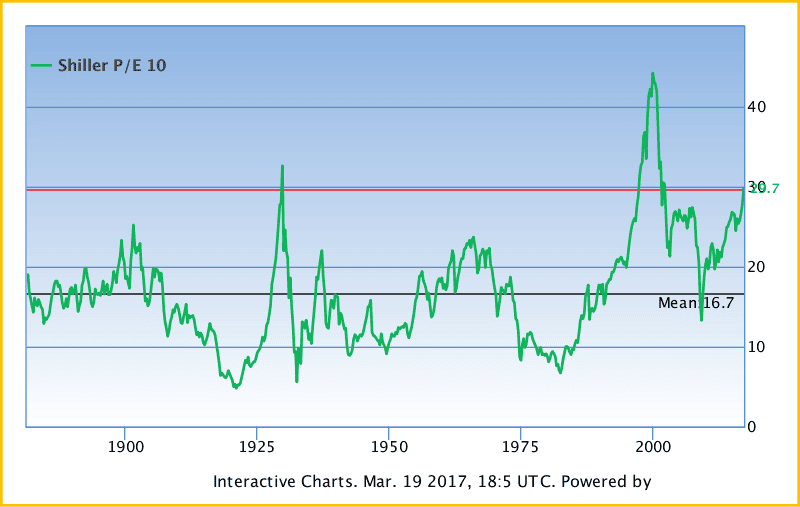

Price-earnings ratios (Shiller PER)

Furthermore an analysis of the historical price-earnings ratios will help us.

To see what returns investors have historically called for, we will take a look at the historical price-earnings ratio of the S&P 500, calculated using the average profits of the last 10 years.

{kind=link}

The price-earnings ratio, as explained above, is approximately the current yield of a shareholder. The interest returns shareholders have historically called for vary greatly . The average PER was approximately 17 (corresponding to a yield of 5.9%), most of the time the PERs quoted around 10-20, equal returns of between 5 and 10% ( reciprocal ).

But companies usually reinvest a portion of their profits and consequently the yields have to be adjusted slightly higher, between about 6 or 7 and just over 10% .

Conclusion

A purely mathematical calculation makes no sense and thus would be more theoretical. But the data compiled and the inspected areas here let us come to a useful assessment of which discount rate could be fair.

- Inflation + interest require about 4 %

- Corporate bonds yield at about 4-7 % or even higher

- Risk bonus derived from historical PER analysis requires about 10 %

So we come to the conclusion that a long-term yield of about 10% – 15% should be a realistic minimum return rate.

For our investment areas we classify as follows:

| Europas | 7,5% |

| Americas | 7,5% |

| Japan | 5,5% |

| Australia | 9,5% |

| Other | 12% |

Actual rates p.a.